Article 4 Explained: What HMO Property Investors Need to Know in Rugby and the West Midlands

If you own - or are thinking of buying - an HMO in Rugby, you've probably heard the words "Article 4" being thrown around a lot lately. And if they've made you nervous, that's understandable. New planning rules, a council on the move, and a lot of half-informed opinions circulating online. It's the kind of thing that makes investors pause and second-guess perfectly solid deals.

But here's the thing: Article 4 isn't the end of HMO investing in Rugby or the wider West Midlands. In the right hands, with the right knowledge, it's actually a filter that separates informed investors from the pack. This article will walk you through exactly what's changed, what it means for you, and how to position yourself ahead of the curve.

Project Graham. Photo by Abacus Property Group

So What Actually Is Article 4?

Let's strip this back to basics.

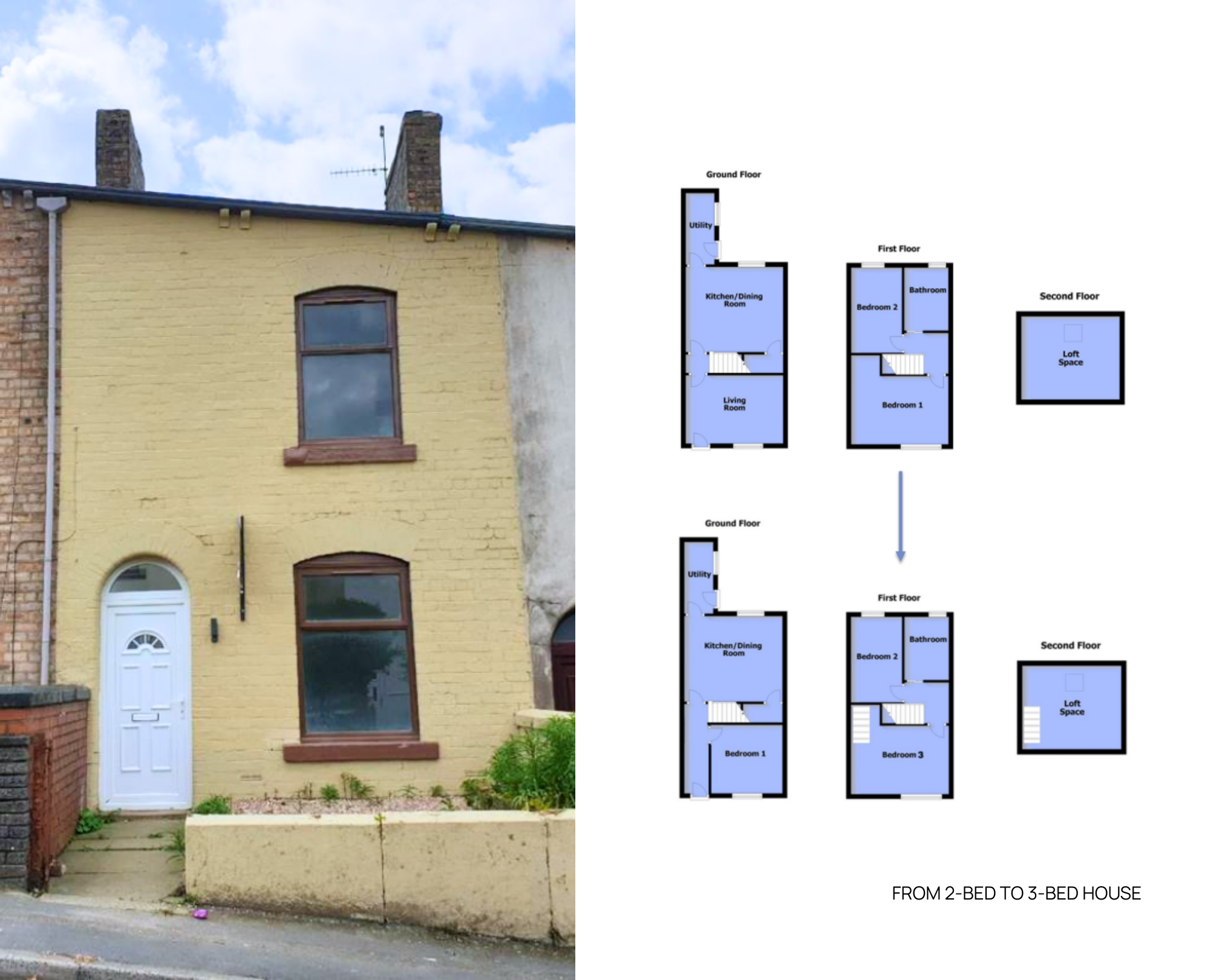

Under standard planning rules in England, converting a regular family home (known as a C3 dwelling) into a small HMO - shared by three to six unrelated people (C4 use class) - doesn't require planning permission. It falls under what's called Permitted Development Rights. You simply do the conversion, notify the council if required, and get on with it.

An Article 4 Direction removes that automatic right. Once one is in place, you need to apply for full planning permission before converting a C3 to a C4 HMO in the designated area. The council can then assess each application on its merits - and, crucially, can say no.

It's worth being clear about what Article 4 does not do. It doesn't make existing, lawfully operating HMOs illegal. It doesn't apply retrospectively. And it doesn't affect large HMOs of seven or more occupants - those have always required planning permission, regardless of Article 4.¹

Project Manor. Photo by Abacus Property Group

What's Happened in Rugby - and When

This isn't a theoretical concern for Rugby investors. It has already happened.

Rugby Borough Council confirmed its Article 4 Direction on 25 September 2024, following a consultation period that opened in February of that year.² The Direction came into force on 23 February 2025 - meaning it is live and active right now.³

The Direction applies to five specific wards in the central area of Rugby: **Benn, Coton and Boughton, Eastlands, New Bilton, and Newbold and Brownsover.**⁴

If your target property sits in any of these wards and it's currently a family home (C3), you will now need planning permission before converting it into a small HMO. That's a meaningful change from the process that was in place just months ago.

The council has been transparent about why it acted. Councillor Louise Robinson, portfolio holder for growth and investment at Rugby Borough Council, noted that under the old rules the council had no mechanism to record how many small HMOs were being created or where they were.⁵ The direction is described as "the first step" in a broader approach, with HMO policy expected to be written into Rugby's emerging Local Plan.³

A consultation on the direction received responses that were unanimously in support, including a petition signed by 651 residents from the affected wards.⁶

Project Boughton. Photo by Abacus Property Group

You Already Own an HMO in These Wards - Should You Be Worried?

No - and this is the bit that often gets lost in the noise.

Article 4 Directions are not retrospective. If your property was already operating as a lawful HMO before 23 February 2025, you don't need to apply for planning permission retrospectively.¹ Your existing use is protected (read on below to find out how to certify it).The practical implication is about future conversions, not current ones.

The one caveat worth knowing: if a property was used as a C4 HMO before the direction came into force but has since been empty, it retains its C4 use class - provided no other use has taken place in the interim.¹ So if you've recently acquired a former HMO in one of these wards that's been vacant, you're generally still protected. But it's always worth getting written confirmation from the council's planning team before you proceed.

Protecting your position: Certificate of Lawful Use

If you own an existing HMO in one of the five affected wards and want to put your lawful use beyond doubt — for example, ahead of a remortgage, a sale, or simply for your own records — it's worth applying for a Certificate of Lawful Existing Use or Development (CLEUD) from the Local Council's planning department. A CLEUD is a formal legal document confirming that the property's use as a C4 HMO was lawful at a specific point in time. It doesn't grant permission for anything new; it establishes an evidenced record of your existing use rights.

This can be particularly valuable if your property has changed hands recently, if there have been periods of vacancy, or if you anticipate any future challenge to the property's use class. The application requires evidence — tenancy agreements, utility bills, council tax records, and the like — but the resulting certificate provides a robust, legally defensible position that no amount of verbal assurance from the council can replicate.

Project Saint. Photo by Abacus Property Group

Does Article 4 Apply to Larger HMOs?

This is another area where investors frequently get confused.

Large HMOs - those occupied by seven or more unrelated people - fall under what's called Sui Generis use class. These have always required full planning permission, everywhere in the borough, regardless of Article 4.¹ The Direction only affects the C4 small HMO category (three to six occupants).

So if you're developing or acquiring a larger HMO anywhere in Rugby - inside or outside the five affected wards - nothing changes in terms of your planning obligations. You needed permission before, and you still do now.

I Want to Convert a Property in an Affected Ward. What Now?

If your property is in one of the five designated wards and you want to convert it from a C3 to a C4 HMO, here's the process as it stands:

Project Saint. Photo by Abacus Property Group

Step one is to consider getting pre-application advice from Rugby Borough Council's planning team. This is a paid service but gives you a steer on whether your specific proposal is likely to succeed before you commit to a full application. It can save time, money, and frustration.

Step two is to submit a full planning application. The national fee for a change-of-use planning application currently sits at around £586.⁷ Councils typically aim to determine these applications within eight weeks of validation.⁷

Step three is the assessment. The council will consider factors like the concentration of HMOs in the immediate area, impact on parking, the character of the neighbourhood, and whether the proposal meets any emerging local plan policies for HMO distribution.

Step four if permission is granted - is to proceed with conversion, HMO licensing, and lettings as normal. Planning permission and HMO licensing are entirely separate processes; one doesn't replace the other.⁷

Planning for Sui Generis HMOs (seven or more occupants)

If you're planning a larger HMO of seven or more occupants anywhere in Rugby — in or outside the Article 4 wards — full planning permission has always been required, as these properties fall under Sui Generis use class rather than C4. The planning considerations are broadly similar to those for a C4 application, but the council will also scrutinise the scale of the proposal more closely, including its impact on the character of the street and the immediate neighbourhood.

Given the greater complexity and the higher development investment typically involved in a Sui Generis HMO, professional pre-application advice is strongly recommended before committing to a site or acquisition. It's also worth noting that Sui Generis HMOs can be valued on a commercial rather than residential basis by lenders, so specialist HMO finance will be required from the outset.

And if you skip the process altogether? The council can issue an Enforcement Notice requiring you to revert the property back to a single dwelling - at your own cost. In some cases, it can also result in a Breach of Condition Notice or formal prosecution. It's not worth the risk, and with an eight-week turnaround on applications, there's really no shortcut worth taking.

The honest reality is that a well-prepared application in an area that isn't already oversaturated with HMOs has a reasonable chance of success. The council's stated goal is oversight and management, not a blanket ban.³ But you do need to go in with eyes open, proper support, and - ideally - local expertise.

Photo from garringtoncentral.co.uk

What's the Broader Picture Across Warwickshire?

Rugby isn't operating in isolation. Warwick District Council introduced an Article 4 Direction covering six wards in Leamington Spa back in 2012, covering the Brunswick, Clarendon, Crown, Manor, Milverton and Willes wards - one of the earlier adoptions in Warwickshire.⁸ So investors in Leamington have been navigating this landscape for over a decade.

Interestingly, neighbouring authorities like North Warwickshire have assessed the question and, as of their most recent review, opted not to introduce an Article 4 Direction - noting that HMOs in that area represent just 0.1% of housing stock, well below the 0.5% threshold that other councils have used as a trigger.⁹

Across the wider West Midlands, Birmingham has Article 4 Directions in place in several key areas, including parts of Selly Oak — one of the city's highest-demand HMO zones.

The picture across the region, then, is uneven. Some areas are constrained; others remain fully open. Knowing the map - ward by ward - is increasingly non-negotiable for any serious investor.

Left image by Abacus Property Group, Project Railway. Right image by www.rugby.gov.uk

Does Article 4 Kill HMO Yields in Affected Areas?

This is the question investors really want answered. And the answer, broadly, is no - but the strategy has to shift.

Here's the counter-intuitive truth: Article 4 areas often produce better long-term yields for those who are already in them. Why? Because the barrier to new entry rises sharply. Fewer conversions get through planning. Supply tightens. Existing, compliant HMOs become more valuable - both in terms of occupancy rates and rental income, and as assets if you ever choose to sell.

In Rugby itself, well-positioned HMOs in the central wards are generating gross yields in the region of 8–10%, based on typical room rents of £550–£650 per calendar month against purchase prices for suitable terraced stock of £200,000–£250,000.* Across the wider West Midlands, HMO rental yields average around 7.63%, compared to single-let buy-to-let yields that typically sit around 3.5–5%.¹⁰ In Birmingham's strongest HMO postcodes, yields push up to 8.5%.¹¹ That premium exists partly because Article 4 constraints limit competition in certain areas.

The West Midlands as a whole remains one of the strongest regions in England for HMO investment, and demand continues to be driven by a growing young professional population, strong university presence, and an acute shortage of affordable single-unit rental stock. Birmingham alone has 80,000 students across eight universities, and nearly 44% of the city's population is under 30.¹² These aren't temporary demand drivers - they're structural.

The Smart Move for Investors Right Now

Photo by rugbyobserver.co.uk

The investors who come unstuck with Article 4 are the ones who didn't know about it until after they'd exchanged. The ones who thrive are those who've built the check into their acquisition process from day one.

For anyone targeting Rugby specifically, that means two things. First, check whether your target property sits within the five affected wards before you make an offer - not after. Second, if it does, factor the planning application into your timeline and budget. Eight weeks to a decision, £586 in fees, and - with the right application - a very real chance of approval.

For investors looking across the wider West Midlands, the lesson from Rugby is to treat Article 4 status as a due diligence item on every deal, in the same category as title checks and survey results. It's not a reason to avoid HMOs - it's a reason to understand them better than the next person in the room.

At Abacus Property Group, we source, develop, and manage HMOs across Rugby and the West Midlands. Every deal we work on goes through compliance checks as standard - including Article 4 status, licensing requirements, and planning history. If you want to know whether a specific property or area works for your investment goals, get in touch with our team.

Key Takeaways

Rugby's Article 4 Direction came into force on 23 February 2025, covering the Benn, Coton and Boughton, Eastlands, New Bilton, and Newbold and Brownsover wards.

It requires planning permission for any new C3 to C4 HMO conversions in those wards — existing lawful HMOs are unaffected.

Existing HMO owners in affected wards should consider applying for a Certificate of Lawful Existing Use or Development (CLEUD) to formally evidence and protect their use rights.

Large HMOs (Sui Generis, 7+ occupants) have always needed planning permission everywhere — Article 4 changes nothing there. Sui Generis HMOs also require specialist finance and are valued on a commercial basis.

The planning application process takes around eight weeks, with a fee of approximately £586.

Rugby HMOs are generating gross yields in the region of 8–10%;* HMO yields across the West Midlands average 7.63%, significantly outperforming standard buy-to-let.

Warwick District (Leamington Spa) has had Article 4 in place since 2012; North Warwickshire has opted not to introduce it.

Always check Article 4 status before acquisition, not after.

* Rugby yield figure — editorial note: The 8–10% gross yield range is derived from Rugby HMO market listings (CV21 postcodes, 2024–2025) and is illustrative. Actual returns depend on individual property variables including purchase price, room count, local room rents, void periods, and management costs. This figure has not been drawn from a single published source. If preferred, this can be replaced with a citation once a suitable local agent report or dataset is available. Suggested footnote wording: Based on market evidence from Rugby HMO listings, 2024–2025; figures are illustrative and subject to individual property variables. Always seek independent financial advice before making investment decisions. Abacus Property Group delivers end-to-end investor developer services across Rugby and the West Midlands - from deal sourcing and planning to development, lettings, and management. Talk to us about your next HMO project.

References

¹ Rugby Borough Council, Article 4 Direction — Houses in Multiple Occupation (HMOs), rugby.gov.uk, confirmed 25 September 2024; in force 23 February 2025. See also Town and Country Planning (General Permitted Development) (England) Order 2015.

² Rugby Borough Council, Notice of Confirmation of Article 4 Direction — HMOs, September 2024, rugby.gov.uk

³ Propertymark, Tough Restrictions on Small HMOs, propertymark.co.uk, 2024

⁴ Rugby Borough Council, Council Set to Confirm New Planning Rules for Small HMOs, rugbytowncentre.org.uk, September 2024

⁵ Property118, Rugby Borough Council Implements Powers to Control HMOs, property118.com, October 2024

⁶ The Rugby Observer, Restrictions on Houses in Multiple Occupation in Rugby Set to Tighten, rugbyobserver.co.uk, September 2024

⁷ GOV.UK, Fees for Planning Applications, gov.uk/guidance/fees-for-planning-applications, updated April 2025; Planning Portal, Application Fees England from 1 April 2025.

⁸ Warwick District Council, HMO Article 4 Direction — FAQs, warwickdc.gov.uk

⁹ North Warwickshire Borough Council, HMO Article 4 Report, northwarks.gov.uk

¹⁰ HMO Checker, 5 Top Cities for HMO Investment in the UK 2025, hmochecker.co.uk, January 2025

¹¹ Parata Property, Navigating the UK HMO Property Market in 2025, parataproperty.co.uk

¹² Invest in HMOs, HMO Investment in Birmingham in 2025, investinhmos.co.uk, 2025